Where’s the home insurance apocalypse they’ve been promising?

Read to the bottom for product safety bangers.

Good Morning!

I missed yesterday’s newsletter. I could give you an excuse, but that would just be a waste of everyone’s time, right? So let’s just move on to today’s newsletter…

-Mike

When I was 24 I really wanted to work in Congress. So after some furious door pounding, I finally found a Congressperson willing to hire me. The problem was that the job paid a measly $26,000, barely enough to pay for my apartment, car payment, and food. The cost of living in D.C. was so high that paying for health insurance was more than I could bear at the time. I took the job but decided to pass on paying for Congressional employee health insurance.

At 24, that seemed like a pretty smart bet. I was healthy, never needed any medications in my life, and was a physically risk averse guy. Things worked out well.

Until I broke my arm in a Congressional League softball game.

It was a freak accident. Playing first base, I reached out low to catch a throw from home plate, the runner came in fast and kicked my forearm with his shin. It was a beer league, so I’d had a couple already and didn’t really feel it right away. But then my arm started to hurt like mad, swell up…and I was off to the emergency room. You know what happened next.

Living without insurance of any kind is generally a bad bet. That’s why insurance works: Over years one gradually pays the expected cost of a disaster so that over time the cost doesn’t hurt much, and if one does meet disaster, the disaster’s financial impact doesn’t hurt too much. It’s a distribution of risk for both the insured and insurer.

Anyway, that’s what people in Florida, California, Louisiana, and all kinds of other disaster-prone places (like new disaster entrant, Hawaii) are doing these days: Living without insurance, because the cost of living doesn’t leave any room for paying the exceedingly high cost of insurance, which is twice the national average in California, and four times the average in Florida.

That’s because – and I’ve written about this a few times here – the damage caused by wildfire, hurricane wind, and hurricane flooding is so high that insurers are jacking up rates to make up for their losses, or often pulling up stakes entirely, because they don’t see how they can’t afford to do business in disaster-prone areas.

Close readers of this newsletter may also know that I’m fascinated with secondary effects, changes to a system that are the result of a primary change. Like that Walmart would never have happened without the popularization of automobiles and suburbs.

You could say that home insurance spikes are a secondary effect of climate change: Hurricanes get bigger and more frequent, disasters get bigger, insurers end up having to pay more.

So, if you’re not reading this from a disaster-prone area, you’re probably thinking something along the lines of, “Geez, that sounds terrible! I wouldn’t buy a house there!”

But apparently that’s not what’s happening. According to a survey of homebuilders from John Burns Research & Consulting, the vast majority of home sales in Florida and California are not impacted by rising insurance rates. There are plenty of analysts saying things like, “at some point”, but it seems that the bargain basement cost of federal flood insurance, as well as state-operated insurance schemes in California and Florida are suppressing the true cost of home insurance, and in effect, the value of property.

These state-operated insurers of “last resort” cover their costs by raising state taxes. In Florida, a state with no income tax, it’s paid for with a surcharge to all homeowners insurance, no matter where you live in the state, whether you use the state insurance or not. For the moment, the state insurance is a finger in the dam that’s straining to burst, but it’s hard for the average person to see the overall picture since they’re just experiencing their own personal costs. That could all change though, with just a couple more big hurricanes, forcing states to jack up prices beyond four times the national average to something truly painful.

The latest warning of how things could truly be comes from First Street Foundation, a climate risk modeling non-profit, which says in a recent report that if just flood risk were taken into account, “39 million properties are at high risk of flooding, wildfires, and hurricane winds which have yet to be reflected in the insurance premiums they pay.”

The study has more apocalyptic indicators. Between 2012 to 2016, wildfires caused $8.5 billion in property damage in the United States. From 2018 to 2021 they caused $79.8 billion in damage. “Most alarming is the economic risk in the state of Florida,” says the report, “where current levels of expected annual losses are already over 4 times the economic risk of the rest of the Gulf Coast combined, and account for approximately 73% of all expected damages nationally”

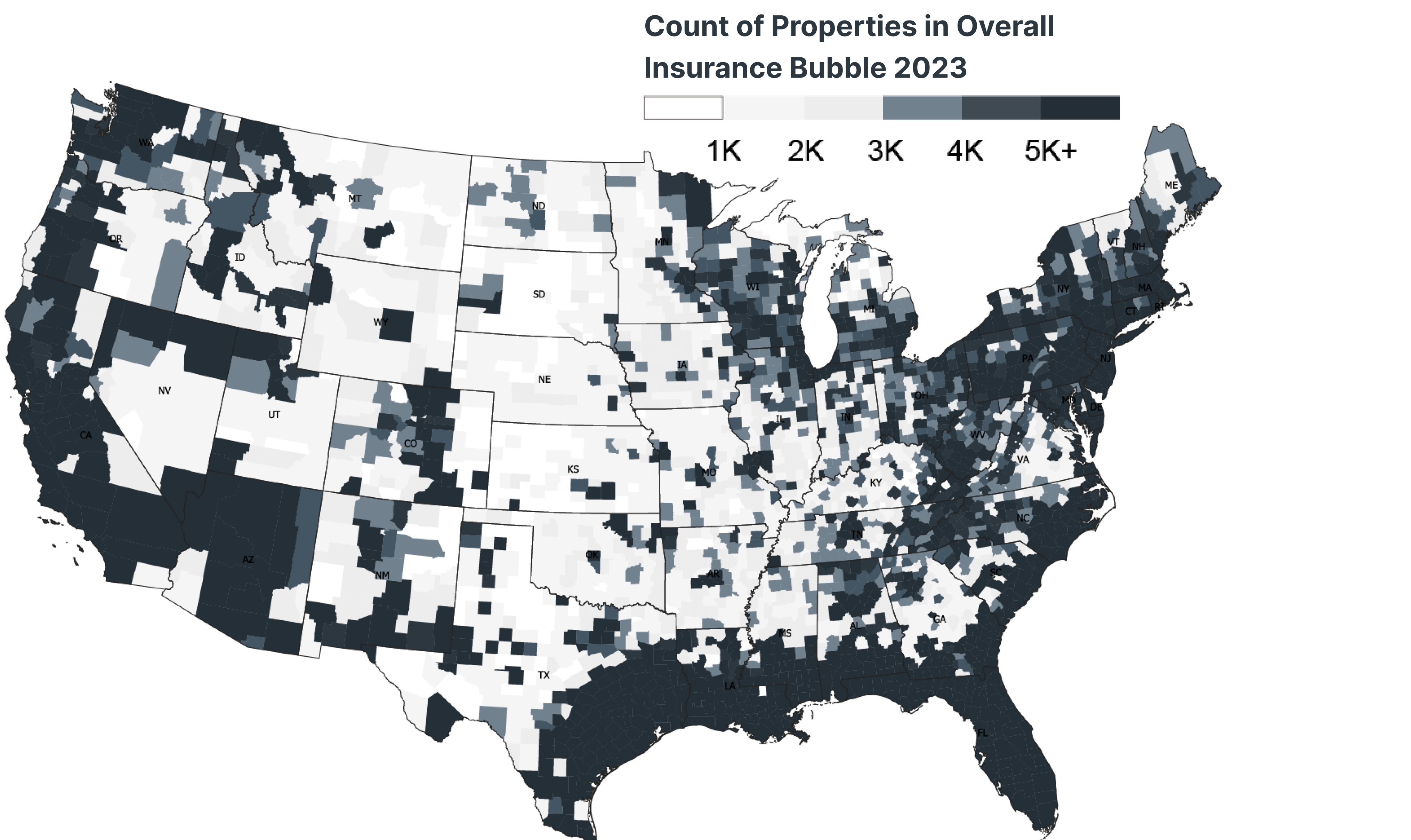

First Street says tens of millions of properties across the country have artificially inflated property values because insurance risk is not properly accounted for (see the map at the top of this newsletter), largely because state-run insurance programs are suppressing those costs.

These state-run organizations are set up to take a loss – which is then paid off through taxes. For instance, Louisiana’s Citizens Insurance, the state-owned insurer of last resort, lost $33.6 million in 2022, a good year. In 2005, losses were so catastrophic, the state issued $978 million in bonds to cover the losses. That sounds like a big number, until you realize that Citizens barely had any policyholders in 2005. Just in the last year, the company reports that the number of policies has tripled, from 47,093 to 154,507. Remember: These are the least insurable homes and businesses, the ones no private company will touch because they are the most likely to go bottom up. We should expect Louisiana to need much more than $978 million when the next big one hits.

So let’s assess: There’s every indication that we should expect more, bigger hurricanes, and more, bigger wildfires. But people are still buying houses in hurricane-prone and wildfire-prone areas. So far state-operated insurers have been skimming off the most risky, most expensive policies, effectively propping up housing markets.

We know that inevitably state legislatures will be called up on to find more money to keep the game going. How will it end? WIth a federal bailout? With hundreds of thousands losing their homes, forced to relocate?

As I learned in a softball game, it’s a bad bet to go without insurance. But our worsening climate is like getting repeatedly whacked with a softball bat – while your insurer contemplates skipping town.

You made it to the bottom! The U.S. Consumer Product Safety Commission released a hip-hop album of product safety bangers. Really. And actually, they’re not that bad. Their “Despacito” ripoff, "Se Pon Caliente” is perfect.

Thank you for reading Heat Rising. This post is public so feel free to share it.